For many business owners, chargebacks have become one of the most frustrating costs of accepting credit cards. What was originally intended as a consumer protection mechanism has evolved into a growing challenge for restaurants, retailers, medical offices, service providers, and eCommerce merchants alike. Beyond the loss of a sale, chargebacks often result in additional fees, lost inventory, increased administrative work, and, in extreme cases, higher processing costs or scrutiny from payment processors.

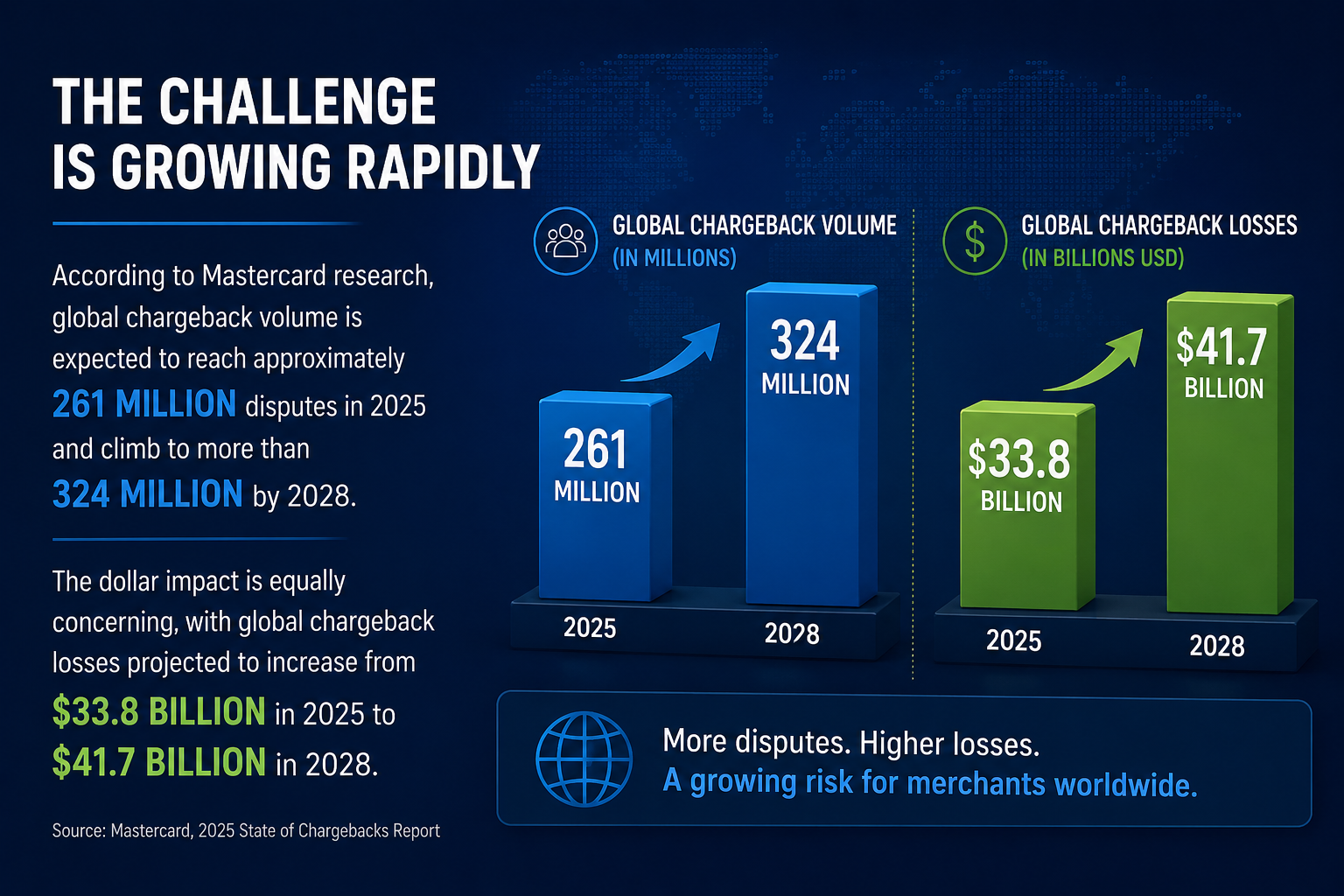

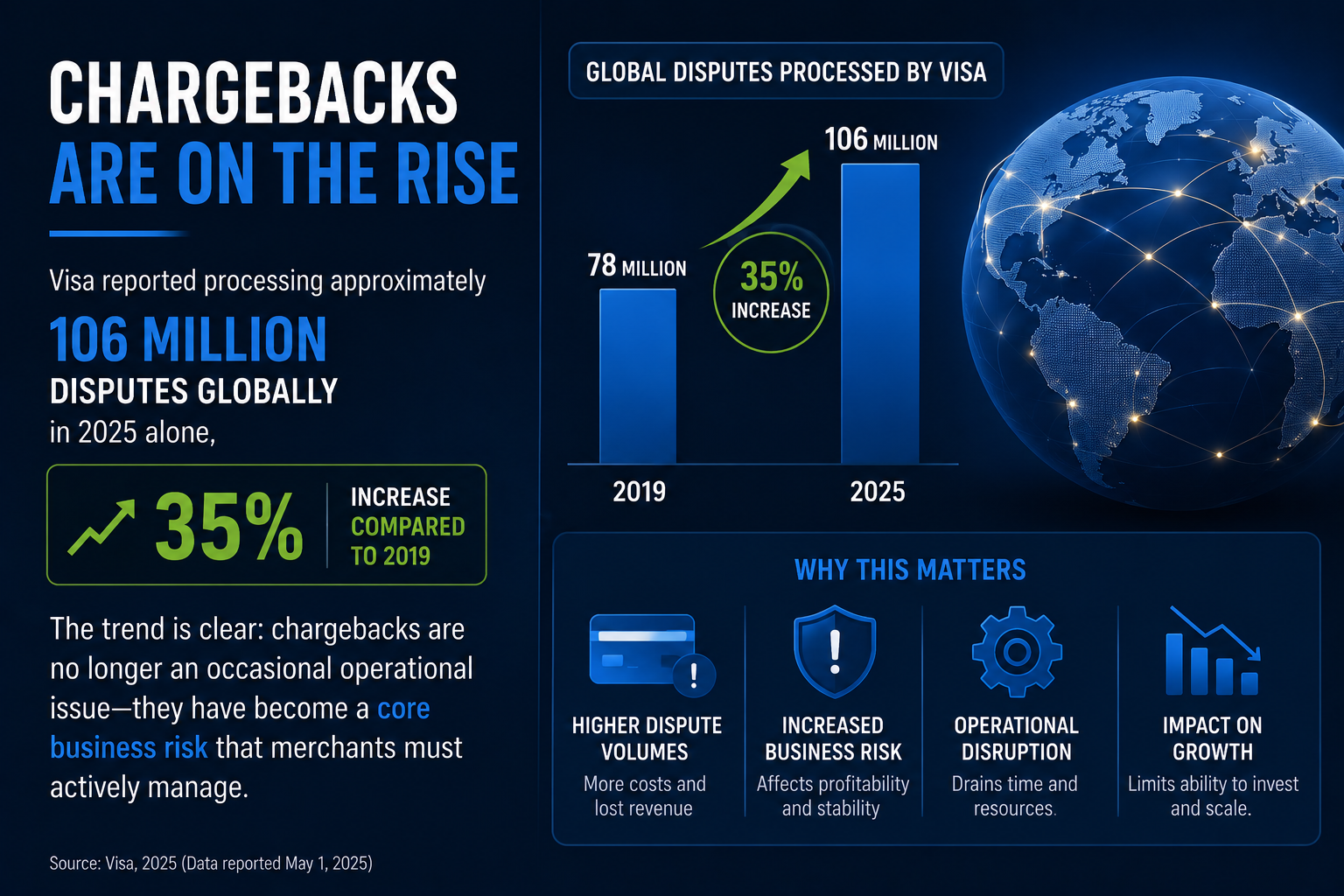

Unfortunately, chargebacks are becoming more common. As consumers increasingly rely on credit cards, mobile wallets, and online purchasing, the opportunities for disputes have expanded as well. Industry analysts estimate that merchants lose billions of dollars annually to chargebacks, with a significant percentage of those disputes stemming not from criminal fraud, but from what the industry refers to as “friendly fraud”—situations where legitimate customers dispute valid transactions.

The reality is that many chargebacks can be prevented long before they occur. By understanding why disputes happen and implementing a few proactive measures, businesses can dramatically reduce their chargeback exposure while improving the customer experience.

Prevention Starts at the Point of Sale

One of the most effective ways to reduce chargebacks is by creating a transparent transaction experience from the very beginning. Customers should clearly understand what they are purchasing, how much they are paying, and who they are paying.

Surprisingly, something as simple as a confusing billing descriptor can trigger a chargeback. If the business name appearing on a customer’s credit card statement differs significantly from the name on the storefront, website, or receipt, the customer may assume the transaction is fraudulent. Ensuring that billing descriptors accurately reflect the business name can eliminate a significant number of unnecessary disputes.

Providing detailed receipts also plays an important role. Whether delivered via email, text message, or paper receipt, customers should have clear documentation showing the date, amount, and details of their purchase. Digital receipts are particularly valuable because they create a permanent record that customers can easily reference later.

For service providers, transparency extends beyond the payment itself. Clear service agreements, signed treatment authorizations, cancellation policies, and documented customer approvals can significantly reduce misunderstandings that often lead to disputes.

The Growing Threat of Friendly Fraud

One of the fastest-growing chargeback trends is friendly fraud. Despite its name, there is often nothing friendly about it.

Friendly fraud occurs when a legitimate customer disputes a valid transaction. In some cases, the customer may genuinely forget making the purchase. In others, the dispute may be intentional. A customer orders food, receives the meal, and later claims it never arrived. A consumer purchases clothing online, keeps the merchandise, and disputes the charge. A cardholder signs up for a subscription, forgets about it months later, and reports the charge as unauthorized.

Because these disputes often involve valid transactions, they can be particularly difficult for merchants to identify and combat.

The best defense against friendly fraud is documentation. Detailed receipts, delivery confirmations, signed agreements, customer communications, and transaction records create a paper trail that can be used to challenge invalid disputes. Businesses that maintain thorough records are often far more successful when responding to chargebacks than those that rely solely on transaction data.

Why EMV and Contactless Payments Matter

Technology has played a significant role in reducing certain types of payment fraud. Chip-enabled EMV transactions and contactless payments provide stronger security protections than traditional magnetic stripe transactions or manually entered card numbers.

Technology has played a significant role in reducing certain types of payment fraud. Chip-enabled EMV transactions and contactless payments provide stronger security protections than traditional magnetic stripe transactions or manually entered card numbers.

For restaurants and retailers, modern payment devices that support EMV and contactless transactions are no longer simply a convenience feature. They have become an important component of a comprehensive chargeback prevention strategy.

Online Merchants Face Unique Challenges

Businesses that accept payments online face a different set of risks because the card is never physically present during the transaction. Without the ability to verify a physical card or customer, online merchants must rely on additional fraud prevention tools.

Address Verification Service (AVS), CVV verification, device fingerprinting, and fraud monitoring tools can help identify suspicious transactions before they become chargebacks. Merchants should pay particular attention to orders involving mismatched billing and shipping addresses, unusually large purchases, or multiple transactions originating from the same device within a short period.

While these precautions may occasionally require additional verification steps, they often prevent much larger losses down the road.

Customer Service May Be Your Best Defense

One of the most overlooked chargeback prevention tools is excellent customer service.

Many chargebacks occur because customers cannot quickly resolve an issue with the merchant. When customers feel ignored, frustrated, or unable to obtain a refund, they frequently turn to their bank instead.

Responding promptly to customer concerns, maintaining accessible support channels, and resolving issues before they escalate can dramatically reduce disputes. In many situations, issuing a refund or store credit is significantly less costly than fighting a chargeback and risking additional fees.

Businesses that make it easy for customers to communicate often discover that many potential disputes never materialize.

Industry-Specific Considerations

Industry-Specific Considerationscan reduce disputes by providing itemized receipts, retaining signed receipts for larger transactions, clearly disclosing service fees, and utilizing tableside payment technology whenever possible. The more transparent the transaction process, the less likely customers are to question charges later.

Retail merchants benefit from clearly posted return policies, surveillance footage at checkout areas, detailed product descriptions, and delivery confirmation for shipped merchandise. These measures provide valuable evidence if a dispute occurs.

Service providers such as medical offices, veterinary clinics, contractors, and professional practices should prioritize signed agreements, treatment authorizations, appointment confirmations, and detailed documentation of services performed. Because these businesses often sell expertise rather than physical products, maintaining comprehensive records is particularly important.

What to Do When a Chargeback Happens

Even the most diligent businesses will occasionally face chargebacks. When they occur, speed matters

Merchants should immediately review the dispute reason code, gather all supporting documentation, and submit a response within the required timeframe. Waiting too long often results in an automatic loss, regardless of the strength of the evidence.

Successful responses typically include receipts, invoices, signed agreements, proof of delivery, customer communications, and any other documentation demonstrating that the transaction was legitimate.

The stronger the documentation, the greater the likelihood of a favorable outcome.

Final Thoughts

Chargebacks are no longer an occasional inconvenience. For many businesses, they have become a recurring operational challenge that directly impacts profitability. However, the majority of disputes do not happen without warning. They are often the result of communication gaps, documentation shortcomings, unclear billing practices, or preventable fraud.

By focusing on transparency, customer service, secure payment technology, and thorough recordkeeping, merchants can significantly reduce their exposure to chargebacks and protect revenue that would otherwise be lost.

At AerPay, we help businesses implement payment solutions designed to reduce fraud, improve transaction visibility, and create a smoother payment experience for both merchants and customers. In today’s payments environment, preventing chargebacks isn’t just about winning disputes—it’s about stopping them before they happen.

If you are ready to scale AND grow your business. We can make that happen. contact us today.