Day: June 1, 2026

-

Merchant Account Denied? Here’s How to Get Approved and Keep Your Business Moving

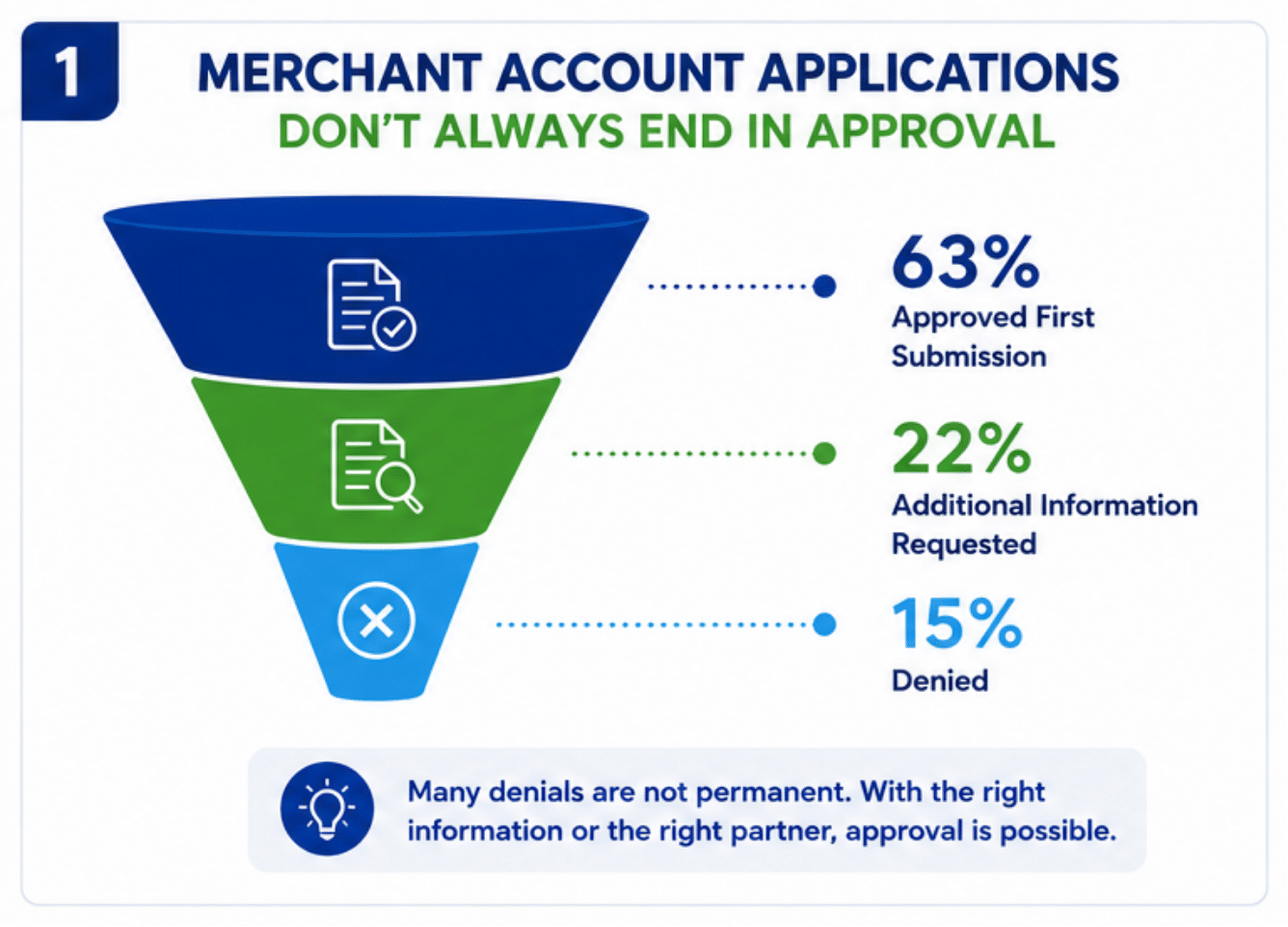

Receiving a merchant account denial can feel like a major setback. Without the ability to accept credit and debit cards, businesses can quickly find themselves facing cash flow challenges, lost sales, and frustrated customers. However, a declined application doesn’t necessarily mean there’s something wrong with your business. In many cases, it simply means the acquiring bank or processor needs additional assurances before approving your account.

In fact, merchant account denials are more common than many business owners realize. Underwriting standards have become increasingly sophisticated as banks work to combat fraud, manage chargeback exposure, and comply with evolving regulatory requirements. Understanding why applications are denied and knowing how to respond can significantly improve your chances of getting approved.

Why Merchant Accounts Get Denied

When a bank evaluates a merchant account application, its primary concern is risk. Every transaction processed through the account ultimately creates financial liability for the acquiring bank. If a business experiences excessive chargebacks, fraud, or financial instability, the bank may be responsible for covering losses.

As a result, underwriters carefully review several factors before making an approval decision. Common considerations include:

- Business type and industry classification

- Personal and business credit history

- Chargeback history

- Processing volume projections

- Website compliance and transparency

- Financial stability

- Identity verification and documentation

Many business owners are surprised to learn that simple administrative issues can trigger a denial. An outdated address, missing documentation, inconsistent website information, or incomplete application details may raise concerns during underwriting.

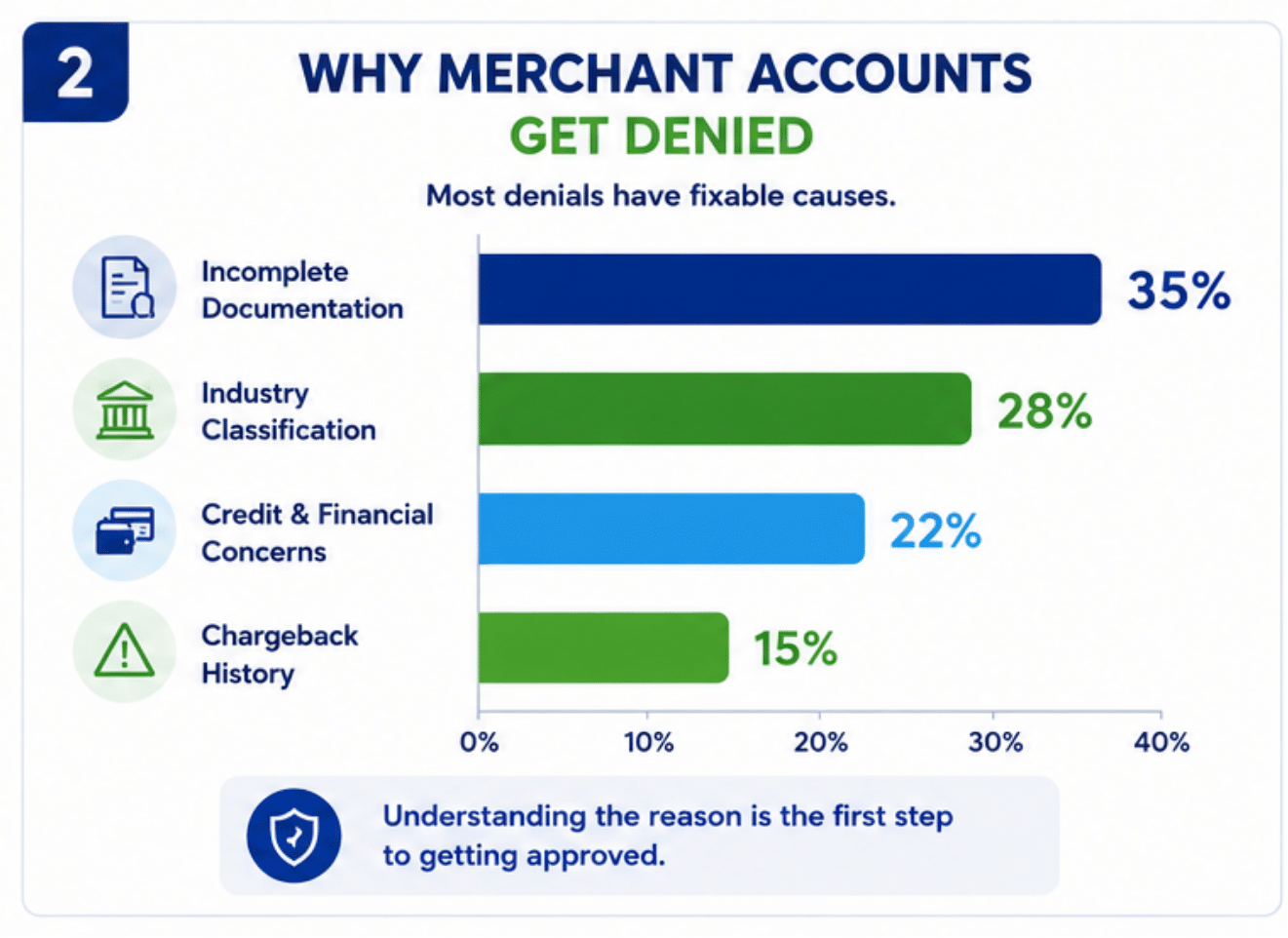

The Most Common Reasons Applications Are Rejected

While every processor has its own risk guidelines, most denials fall into a handful of categories.

Incomplete or Inconsistent Information

One of the most common causes of rejection is inconsistent information across business records, websites, licenses, and application documents. If an underwriter cannot easily verify your business, the application may be declined pending further review.

Before applying, ensure your website, business registration, tax records, and application all reflect the same information.

Industry Risk Classification

Some industries naturally experience higher rates of fraud, disputes, or regulatory scrutiny. Businesses in sectors such as CBD, subscription services, travel, firearms, gaming, and certain eCommerce categories may be classified as higher risk regardless of their actual performance.

This doesn’t mean approval is impossible. It simply means you may need a processor that understands your specific industry and has banking relationships designed to support it.

Credit and Financial Concerns

Banks want confidence that a merchant can cover refunds, disputes, and operational expenses. Significant credit issues, recent bankruptcies, or weak cash reserves may trigger additional scrutiny.

Strong bank statements and a documented operating history can often help offset concerns about credit scores.

Chargeback History

Excessive chargebacks remain one of the biggest red flags in payment processing. Businesses that exceed card brand monitoring thresholds may face account restrictions, reserves, or outright denials.

If your business has experienced chargeback issues in the past, be prepared to explain what corrective actions have been implemented.

What To Do After a Denial

If your application is denied, avoid the temptation to immediately submit multiple applications to different providers. Doing so without addressing the underlying issue can create additional underwriting concerns.

Instead, take a methodical approach.

Step 1: Request Specific Feedback

Ask the processor why the application was declined. Some denials are policy-based, meaning the processor simply doesn’t support your industry. Others are data-driven and may be resolved through additional documentation or clarification.

Understanding the reason is the first step toward fixing the problem.

Step 2: Review Your Online Presence

Your website serves as an important underwriting tool. Ensure that it includes:

- Clear contact information

- Privacy policy

- Refund policy

- Terms and conditions

- Accurate product or service descriptions

Processors want to see a legitimate, transparent business operation.

Step 3: Gather Supporting Documentation

Additional financial statements, bank records, licenses, invoices, supplier agreements, and processing history can often strengthen an application.

The more clearly you can demonstrate stability and legitimacy, the more comfortable underwriters will be.

Step 4: Address Chargeback and Fraud Concerns

If chargebacks contributed to the denial, focus on reducing future risk. Clear customer communication, improved billing descriptors, delivery confirmation, fraud monitoring, and dispute management processes can all help strengthen your profile.

Step 5: Work With a Processor That Understands Your Business

Not every processor serves every industry equally well. Some banks simply don’t have the appetite for certain business models, while others actively support them.

Finding a payments partner with experience in your industry can often make the difference between approval and rejection.

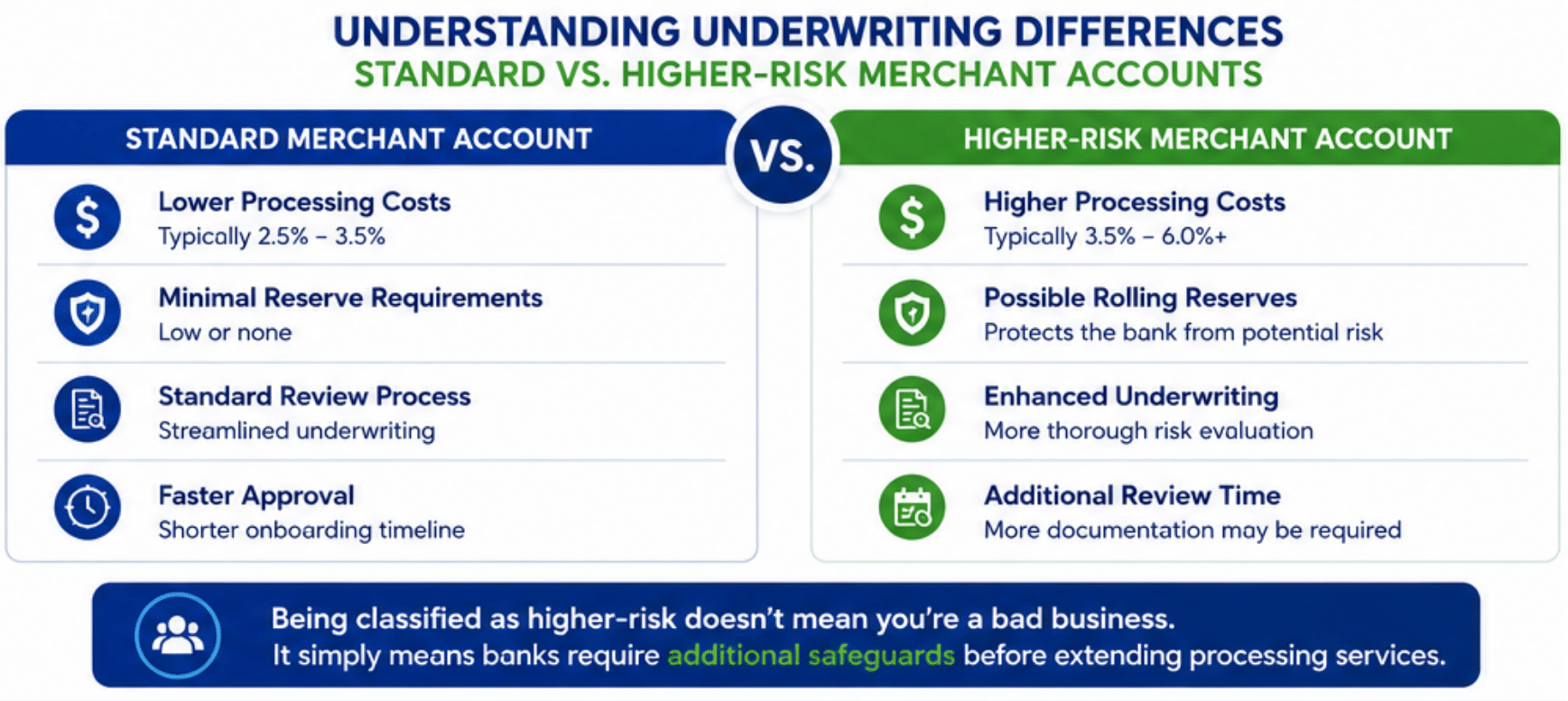

High-Risk Doesn’t Mean Bad Business

Many successful businesses are classified as high-risk. The designation often reflects industry characteristics rather than company performance.

Restaurants, medical practices, contractors, retailers, automotive businesses, subscription services, and eCommerce merchants can all encounter unique underwriting challenges depending on their payment mix and transaction profile.

The key is finding a processor that understands how your business operates and can present your application appropriately to banking partners.

Looking Beyond Approval

Getting approved is important, but it’s only part of the equation.

Many merchants focus exclusively on obtaining an account while overlooking the long-term cost of accepting payments. Processing expenses continue to rise, making it important to evaluate strategies that improve profitability once the account is active.

This is one reason many businesses are exploring options such as ACH acceptance, integrated payment technology, modern POS systems, and Dual Pricing programs.

AerPay’s Aer0 Dual Pricing allows businesses to clearly display both cash and card prices, creating greater transparency while helping offset payment acceptance costs. For many merchants, it has become an effective way to manage expenses without sacrificing customer convenience.

Partnering for Long-Term Success

A merchant account denial should be viewed as a hurdle—not a dead end.

Most denials can be resolved through better documentation, improved compliance, stronger fraud controls, or by working with a processor that better understands your business model.

At AerPay, we help businesses navigate the approval process while identifying payment solutions that support long-term growth. Whether you’re opening a new business, switching processors, or overcoming a previous denial, having the right payments partner can make all the difference.

Getting approved is the goal today. Building a stronger, more profitable payment strategy is the goal for tomorrow.

If you are ready to scale AND grow your business. We can make that happen. contact us today.

Merchant account denied? Learn the most common reasons applications are rejected, what steps to take next, and how to improve your chances of approval with the right payment processing partner.